Most people believe their UK taxes go towards hospitals, lighting, bin collection, pensions and a plethora of other public services. In fact ALL TAXES (Including fines) go to parliament’s Consolidated Fund of which 5-10% finances illegal wars via the MOD. These foreign wars have cost the UK taxpayer £1.2TN since 2001 and have killed 2M people (6M since WWII).

It is a criminal offence in this country to pay tax if any of it is used to fund genocide, murder or any criminal activity as per the 1945 UN Charter, Rome Statute of the International Criminal Court, Terrorism Act 2000 and The Nuremberg Code. You can therefore put all taxes and fines into a Trust (as the oligarchs and many MPs do) with the Treasury as Primary Beneficiary. You have therefore paid your tax, and the government cannot get your money until they can prove that none of it will be used for war or acts of terrorism.

Tax ‘rebellion’ has been the single most important component underlying all successful rebellions in history. Magna Carta started with a tax rebellion, the English Civil War, American War of Independence, French & Russian Revolutions, Gandhi’s Salt Tax Rebellion, the Glasgow Women’s Rent Strike in 1915 and the Poll Tax.

Wilful refusal to pay tax may get you into hot water. But there is a way you can withhold tax that you believe will be spent on criminal purposes, such as the act of funding wars, including genocide, ethnic cleansing and crimes against humanity. It is the same route oligarchs and MPs use to avoid tax. Your aim however is not to avoid tax, but to ensure that any taxes collected by the government are used responsibly and if not, then you have the right to spend your tax in ways that benefit your local community.

Every human being has a duty

in law to refuse to pay their government’s orders if those orders are manifestly illegal – Nuremberg War Crimes Tribunal

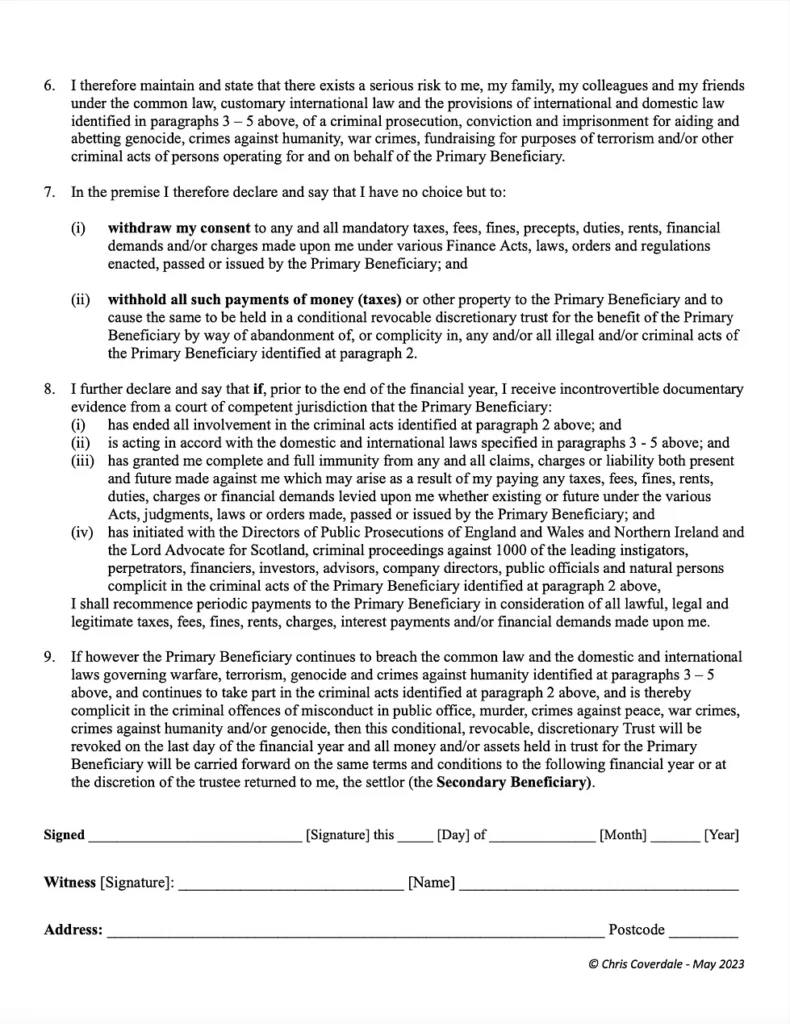

When Is It A Crime to

Collect or Pay Tax?

It’s down to each of us to illegally pay,

or lawfully withhold tax.

The choice is ours.

Most people in Britain never think to ask or answer this question because we make the assumption that our governments use our money to pay for the essential services we need to run the country, such as health, education, defence, the justice system etc.

We also assume that everyone who benefits from these services has a duty to pay for them, and if you fail to contribute your fair share of taxes, you are not only being unfair to everyone else, but you can be arrested and imprisoned for tax evasion.

So how on earth can it be a crime to collect or pay tax?

The answer may be easier to identify if we pose the question in a different way:

When is it a crime for one person to hand over money to another?

The answer to this question is when you know or have reasonable cause to suspect that the other person is intending to use the money for any criminal purpose, such as buying weapons or poison to kill a person, insider dealing on a Stock Exchange, funding a fraud or robbery or financing a terrorist attack. There are numerous ways in which one can commit a crime by handing over money to another person or organisation. It all depends on knowing how the money will be used after it leaves your possession.

In law, it is a statutory criminal offence in Britain to hand over money to a person or organisation if you have reasonable cause to suspect that it may be used for a criminal purpose, such as funding terrorism, war or genocide? In such cases, the person who hands over the money, knowing that it may be used for a criminal purpose, is complicit in the crime and can be prosecuted and imprisoned for aiding and abetting the crime.

So it is important to be clear about the use to which your money will be put BEFORE you hand it over. If you have any suspicion whatsoever that your money could be used to fund a criminal enterprise of any sort, you must check (it’s called due diligence in the financial world) that none of your money will be used in future for a criminal purpose.

So how does this apply to individuals or businesses collecting or paying tax?

The principle is the same. If a taxpayer hands over money to a tax collector such as a council, HMRC, the DVLA or a business charging VAT, knowing that the money will go to the Treasury and some of it will be passed to the Ministry of Defence to buy guns or explosives for use by HM forces to murder people in another country, he or she is complicit in the murders and can be prosecuted alongside Britain’s leaders, for funding terrorism and aiding abetting murder, a crime against humanity or genocide.

But surely waging war and paying military forces to fight an enemy is lawful?

No, it isn’t. War was outlawed in 1928 when we signed and ratified the General Treaty for the Renunciation of War, which is often referred to as the Kellogg Briand Pact. So it is never legal, lawful or legitimate to wage war, or to fund war. The only occasion in international law when the use of armed force is lawful is when a State is under attack by the armed forces of another State and needs to defend itself and repel its attackers. So anyone who takes part in a war of aggression on the side of the aggressor, including those who provide the means, money or materials for the commission of the crime, commits the world’s worst crimes and is liable for arrest and prosecution for complicity in murder, war crimes, crimes against humanity, or genocide.

In 1945, the British government signed and ratified the UN Charter, agreeing on behalf of the British people never to wage war, never to threaten or use force, never to harm or kill people because of their nationality, never to interfere in another nations’ affairs, to respect human rights, uphold and enforce the rule of law, settle all disputes peacefully and work together for the benefit of every nation, mankind and the planet.

Unfortunately, UK and US governments never keep their word or stick to these solemn and lawfully binding agreements. It is a little-known fact that British governments have fought 28 illegal wars, causing the deaths of at least 6 million people since 1945. Since 2001, British governments have spent £1.2 trillion of taxpayers money fighting or supporting seven illegal wars against smaller, weaker, undefended nation states, killing 1.2 million adults and 600,000 children, injuring many more and driving 15,000,000 refugees into exile and destitution.

Not one of our victims was allowed to defend themselves and their families in court before they were summarily executed by order of our leaders. All this, from a nation that likes to think of itself as a civilised, law-abiding exemplar of justice, fair play and the rule of law. Nothing could be further from the truth.

So how does this apply to the collection of payment of council tax? Surely this money is used solely on local services to pay for the police schools, lighting the roads, taking away rubbish etc?

No, not at this stage. The truth is that all the money that council collects in council tax, business rates, rents, charges, fees, fines etc is paid initially into Parliament’s Consolidated Fund. All our taxes go into one pot. The important facts that every taxpayer needs to know is what happens to the money next? How do the government and Parliament spend our money?

Typically they will spend it on the National Health Service, education, welfare, local government, repaying debts and 5-10% of it, 62.5 billion in 2018 is spent by the Ministry of Defence buying bombs, nuclear weapons, missiles, aircraft, tanks, submarines and ships, as well as training and deploying young men and women to conflict areas to use these weapons to attack and destroy enemy targets, but in reality, murdering and maiming thousands of innocent men, women and children as well as destroying their homes, their community infrastructure, their livelihoods, their hopes and their dreams.

In other words, Britain’s taxpayers know that at least 5-10% of the money we pay in tax & fines will be used for the criminal purposes of mass murder and the genocide of innocent people in places such as Iraq, Afghanistan, Libya, Syria, the Yemen, Palestine and other smaller, weaker states around the world – wherever our criminal leaders want to steal resources or forcefully impose our so-called democratic way of life on other people.

So next time that you are asked to pay council tax, VAT, income tax, stamp duty, vehicle tax or any other tax or fine, be aware that of every £100 you pay, you will contribute £5-£10 towards war and the genocide of another group of innocent people.

Every human being has a duty in law to refuse to obey their governments orders if those orders are manifestly illegal.

The answer to the question ‘When is it a crime to collect or pay tax?’ is ‘Whenever we know or suspect that some of our money may be used for a criminal purpose’.

So now, because we know that the government spends 5 to 10% of all its tax income on military affairs, planning to kill and then killing men, women and children, we have a legal duty to withhold all money (taxes) from public authorities in the UK, until the government obeys the law and ends its wars and killings and all preparations for wars.

Only when our wars and war crimes have stopped, when Parliament and the US Congress are acting in full accordance with the UN Charter and the UN Declaration on Principles of International Law and the political, civil, judicial and military leaders responsible for starting the wars and murdering thousands of innocent men, women and children have been arrested and prosecuted for their crimes, can we lawfully recommence the collection and payment of taxes.

So now, it’s down to each of us. To illegally pay or lawfully withhold tax. The choice is ours.

Lawful Tax Resistance

Chris Coverdale, a peace activist, explains the lawful duty to withhold tax

History shows us that the most effective form of resistance to corrupt Government is tax rebellion. Magna Carta, the founding of the United States of America, Indian independence, the end of the Vietnam War and the repeal of the poll tax all came about as a result of tax rebellions – the refusal of the people to pay tax.

Without citizens’ money Governments are powerless.

Today taxpayers have an historic opportunity to engage in lawful tax rebellion. For the first time in history demanding, collecting or paying taxes are criminal offences against both international and domestic law. Under the laws of war, citizens are forbidden from taking part in warfare on the side of an aggressor and they are legally bound to disobey their Government’s orders to support, fund or take part in war or its preparation.

The very essence of the Charter is that individuals have international duties which transcend the national obligations of obedience imposed by the individual State. He who violates the laws of war cannot obtain immunity while acting in pursuance of the authority of the State, if the State, in authorising action, moves outside its competence under international law. (3)

This legal duty to refuse to obey manifestly illegal Government orders, includes tax demands. If a government uses money raised by taxation to wage illegal war or to attack and kill civilians, then under international and domestic law the taxpayer’s normal duty to pay tax is reversed and becomes a duty to withhold tax until their Government obeys and enforces the law.

Each of the wars fought supported or funded by Britain since 2001, in Afghanistan, Iraq, Libya, Syria, Palestine, the Yemen and the Ukraine, was and is illegal, and taking part in such a war on the side of the aggressor States constitutes five of the worst crimes known to mankind – murder, war crimes, crimes against humanity, genocide and a crime against peace.

Not only does the illegal use of armed force violate the Treaty for the Renunciation of War 1928, the UN Charter 1945 and the UN Declaration on Principles of International Law 1970, but by taking part in the killing of 1.4M adults and 600,000 children, leaders and taxpayers of UK, NATO and ISAF States committed the criminal offences of complicity in murder, war crimes, crimes against humanity, genocide and crimes against peace in breach of the Nuremburg Principles and the Rome Statute of the International Criminal Courts.

PAYING TAX IS A WAR CRIME WHEN IT’S USED TO FUND ILLEGAL WAR

Under international and domestic law, every citizen of a government involved in these 21st century wars on the side of the aggressor States who has paid tax knowing that some of the money will finance warfare, is technically an accessory to the war crimes committed by their Government and is criminally liable for prosecution and punishment for complicity in their leaders’ crimes.

Terrorism Act 2000 section 17:

A person commits an offence if he enters into, or becomes concerned in an arrangement, as a result of which, money or other property is made available or is to be made available to another, and he knows or has reasonable cause to suspect that it will or may be used for the purposes of terrorism.

Terrorism = the use of firearms or explosives endangering life for a political cause.

TO AVOID PROSECUTION, DIVERT TAX INTO A TRUST ACCOUNT

It is important to note however that legislators provided relief for taxpayers who were deceived into believing that the wars and the actions of their government were legal. Providing we end our involvement in warfare immediately and withhold all taxes from our government and its agents we will not be punished for paying tax and funding the illegal wars and war crimes.

Taxpayers can prove that they have completely and voluntarily abandoned their support for the crimes of their government by diverting their taxes into a Taxation Trust account held by independent trustees. The funds in a taxation trust account cannot be released to tax collectors until the terms and conditions of the Trust are met in full. In this case, because our leaders and Governments have broken the laws of war, the terms of the Trust Deed must be set to ensure that taxes are not handed over until such time as the Government obeys and enforces the law, ends its participation in war and mass murder, recalls all military forces to their home bases and starts criminal proceedings against those leaders responsible for the wars and war crimes.

I’m often asked whether taxpayers can be prosecuted for withholding their taxes. The answer is “No”, you are upholding and obeying the laws against funding murder, terrorism, war crimes, crimes against humanity and genocide. If you have paid your taxes into a properly constituted Trust and the tax collector has received a copy of the Trust Deed and the lawful redemption criteria it contains, you have paid your tax and you can’t be prosecuted for not paying it.

However, you could be prosecuted as an accessory to war crimes, crimes against humanity and genocide if you continue to pay tax knowing that some of your money will be used by the Government to fund its wars and the murder of innocent men women and children. If you continue to pay taxes, such as income tax, council tax, vehicle tax, VAT, PAYE or corporation tax, or make payments or repay loans to the Government after you’ve been warned that it is a criminal offence to do so, and if our law enforcement authorities enforce the law rather than enforcing government crimes, you could be prosecuted as an accessory to our leaders’ crimes.

COMPEL OUR LEADERS TO OBEY AND ENFORCE THE LAW

By engaging in lawful tax resistance and diverting taxes into trust accounts, taxpayers regain control over their money, their Government and the law. Without the support and consent of the people Governments are powerless.

No longer can they use taxpayers’ funds to wage unlawful wars, murder civilians, bail out the banks, finance fatal toxic inoculation campaigns or support the rich at the expense of the poor. By diverting tax payments into trust accounts we can force our political, civil, judicial and military leaders out of office and into court. By using the law to force Governments to obey the law we engage in a civil obedience campaign.

JOIN THE CIVIL OBEDIENCE CAMPAIGN

Tax rebellion is the single most effective non-violent way of forcing governments to obey the laws of war, but it only succeeds when thousands take part. If most taxpayers continue to pay tax then Governments will continue to wage illegal war. So it is down to each of us to end the carnage. If you want to uphold the law, stop the wars and end the killing, then withhold tax. If you want the wars and the killing to continue, then continue paying tax – the choice is yours.

“War is essentially an evil thing. Its consequences are not confined to the belligerent states alone, but affect the whole world. To initiate a war of aggression therefore, is not only an international crime, it is the supreme international crime differing only from other war crimes in that it contains within itself the accumulated evil of the whole.”

Nuremburg War Crimes Tribunal 1946

If leaders and taxpayers obey the law, nation States can never wage war.

Chris Coverdale

Make War History

October 2023

1 The Nuremberg Principles 1950, The International Convention for the Suppression of the Financing of Terrorism, The Rome Statute of the International Criminal Court, the Terrorism Act 2000, the International Criminal Court Act 2001 and the International Criminal Court [Scotland] Act 2001.

2 The Judgement of the Nuremburg War Crimes Tribunal

3 Nuremburg War Crimes Tribunal 1946

4 UN General Assembly Resolution 2625 (1970).

5 US citizens cannot be prosecuted under the Rome Statute but can be prosecuted for genocide under the

Proxmire Act 1988.

6 Article 2 of the Convention for the Suppression of the Financing of Terrorism

7 Sections 15 – 17 Terrorism Act 2000

8 Summary of the definition of Terrorism from section 1 of the Terrorism Act 2000

9 Article 25.3(f) of the Rome Statute of the International Criminal Court states “a person who abandons the effort to commit the crime or otherwise prevents the completion of the crime shall not be liable for punishment under this Statute for the attempt to commit that crime if that person completely and voluntarily gave up the criminal purpose.”

Ten employees who have their tax deducted at source should give a copy of this article to their employer and ask them to pay all tax payments, including PAYE and NI deductions, into a taxation trust or escrow account. Remind them that should they fail to do so the company directors and business managers will be criminally liable as accessories to war crime.

STEP 1

STOP FUNDING WARS

JOIN THE TAX RESISTANCE

Weapons makers in the US have spent $2.5 billion on lobbying over the past two decades, employing, on average, over 700 lobbyists per year over the past five years. That is more than one for every member of Congress.

While the UK Parliament has never represented true democracy – a Remembrancer sits in Parliament deciding on which laws, statutes and legal instruments best serve the city and not the constituents, as taxpayers we have a voice.

Overnight we have it in our power to

STOP FUNDING ILLEGAL WARS

Crimes against humanity, ethnic cleansing and genocide.

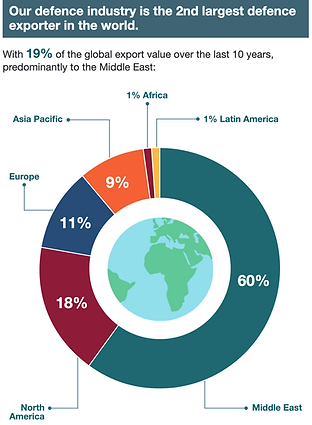

All 230 of our taxes and fines go into Parliament’s

Consolidated Fund

…which then diverts 5-10% of our taxes towards ‘defence’. The cost of defence, which includes preparation for war, illegal munitions, ships, planes, shells etc is currently calculated at £55-80BN annually at an average cost to the taxpayer of £1,875/year since 2021.

It is not defence in the classic sense of protecting the UK from external attacks, but a defence industry, subsidised by the taxpayer at the cost of millions of lives worldwide.

Weapons makers in the US have spent $2.5 billion on lobbying over the past two decades, employing, on average, over 700 lobbyists per year over the past five years. That is more than one for every member of Congress.

While the UK Parliament has never represented true democracy – a Remembrancer sits in Parliament deciding on which laws, statutes and legal instruments best serve the city and not the constituents, as taxpayers we have a voice.

Overnight we have it in our power to

STOP FUNDING ILLEGAL WARS

Crimes against humanity, ethnic cleansing and genocide.

To lawfully withhold Council Tax

and all other taxes & fines, download the DEED of DECLARATION below:

Follow the instructions below detailing how to fill in the DEED and what to do with it afterwards.

In addition, if you have NI and PAYE tax taken at source, you will also need to download the DEED of DECLARATION below.

Follow the instructions below detailing how to fill in the DEED and what to do with it afterwards.

A company can open up a Trust for any of their members or employees to put all their taxes in. The company will only pay the money to the government once the government can prove it is no longer involved in genocide, crimes against humanity, war crimes or other criminal activities for that tax year. If the government is unable to prove this by the end of the tax year, the money goes back to the employee.

Deed of Declaration of Conditional Trust (Companies)

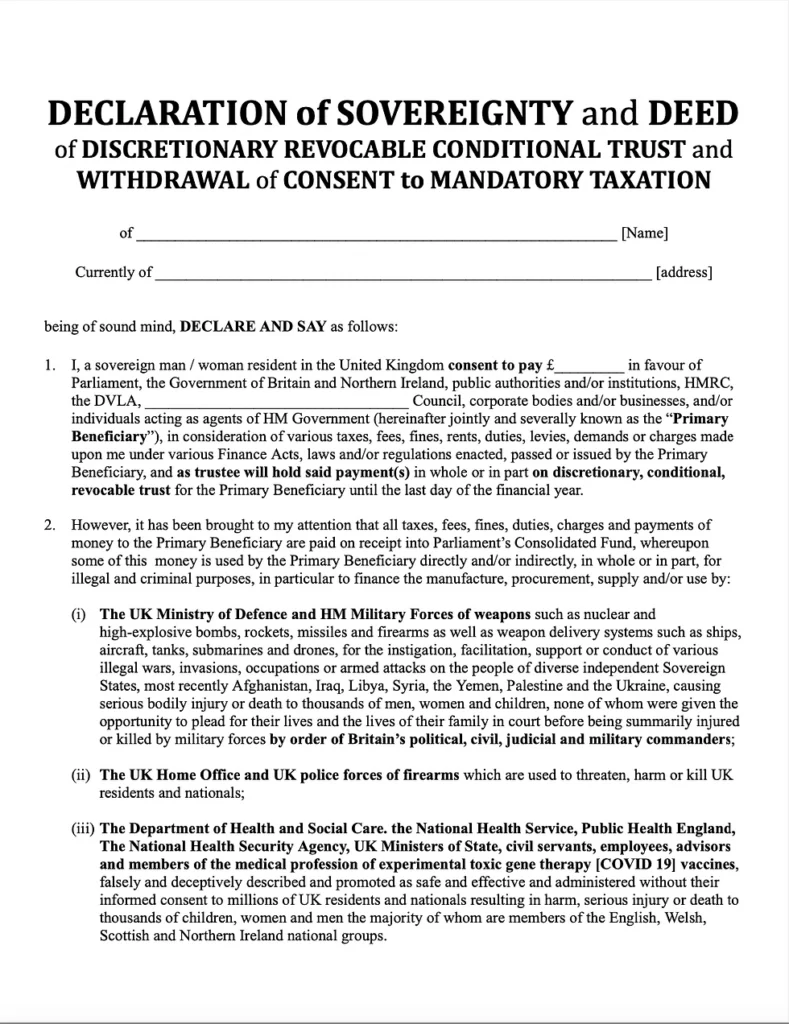

DEED OF DECLARATION OF CONDITIONAL TRUST AND WITHDRAWAL OF CONSENT TO MANDATORY TAXATION

of _____________________________________________________________ [Company Name]

Company Registration Number __________________________

with registered offices at ________________________________________________________________________________

We the directors of the above named company DECLARE and SAY as follows:

1. For many years we have dutifully obeyed the law and fulfilled our obligations to Parliament, HM Government and HM Revenue and Customs [HMRC] to deduct P.A.Y.E. and N.I. contributions from the salaries and wages paid to our employees’ and then to transfer this money together with our employer’s contribution to HMRC.

2. However, it has been brought to our attention that such actions of the company directors and/or managers in collecting money (tax) from employees’ salaries and wages and transferring it to HM Government are unlawful, illegal and criminal under domestic and international law and constitute serious imprisonable offences if a person knows, or has reasonable cause to suspect, that some of the money may be used for criminal purposes such as terrorism, war or genocide. (see paragraphs 6 – 17 below)

3. We were then informed, and have since confirmed, that since 2001 HM Government and our political, civil, judicial, military and corporate leaders have broken the major domestic and international criminal laws signed and ratified by Parliament that govern warfare and the use of armed force. In addition, we confirmed that Britain’s leaders use up to £60bn of UK taxpayers’ money for criminal purposes each year to wage, supply, support or take part in illegal warfare and the mass murder of civilians, most recently in Afghanistan, Iraq, Libya, Syria, the Yemen, the Ukraine and Palestine.

4. We now know that these actions by the military forces of the UK, the USA, Israel and other Governments are criminal and have caused the unlawful deaths of at least 2M men, women and children, have injured many more, have destroyed homes, livelihoods and community infrastructure and have driven 20M refugees into exile and destitution.

5. It is our shared belief that these horrific crimes are amongst the worst ever committed or supported by Britain’s political, civil and corporate leaders and taxpayers, so we have determined, on behalf of our shareholders and employees, to withdraw our consent to mandatory taxation and to take no further part in condoning, supporting or financing war, terrorism or military or medical activities designed to harm and kill human beings.

International law governing warfare, genocide and their funding

6. In 1945 the UK Government signed and ratified the Charter of the United Nations and agreed to be bound by its rules which amongst 109 others

provide that:

- 2.3 All members shall settle their international disputes by peaceful means in such a manner that international peace, security and justice are not endangered.

- 2.4 All members shall refrain in their international relations from the threat or use of force against the territorial integrity or political independence of any state or in any other manner inconsistent with the Purposes of the United Nations.

- 41 The Security Council may decide what measures, not involving the use of armed force, are to be employed to give effect to its decisions.

7. In 1970 the United Nations’ Declarations on Principles of International Law concerning friendly relations and co-operation among States

in accordance with the Charter of the United Nations (UNGAR 2625) came into force. Included in its 42 principles are the following solemn

and binding agreements:

- … a threat or use of force constitutes a violation of international law and the Charter of the United Nations and shall never be employed as a means of settling international issues;

- A war of aggression constitutes a crime against peace, for which there is [individual and joint] responsibility under international law;

- No State or group of States has the right to intervene, directly or indirectly, for any reason whatever, in the internal or external affairs of any other State. Armed intervention and all other forms of interference or attempted threats against the personality of the State or against its political, economic and cultural elements are in violation of international law;

8. In 1998 132 nation States signed the Rome Statute of the International Criminal Court. Currently 125 States, including the UK, have ratified

this international treaty and have agreed to place every resident under the jurisdiction of the International Criminal Court in The Hague for

the criminal offences of genocide, crimes against humanity, war crimes and aggression (added in 2017). Two of its most important articles state:

- 25.3 Individual criminal responsibility In accordance with this Statute, a person shall be criminally responsible and liable for punishment for a crime within the jurisdiction of the Court if that person:

- (a)Commits such a crime [a war crime, a crime against humanity, genocide or aggression], whether as an individual, jointly with another or through another person, regardless of whether that other person is criminally responsible;

- (b) Orders, solicits or induces the commission of such a crime…

- (c) For the purpose of facilitating the commission of such a crime, aids, abets or … assists in its commission…including providing the means for its commission;

- (d) In any other way contributes to the commission … of such a crime …

- (e) … directly and publicly incites others to commit genocide;

- (f) … However, a person who abandons the effort to commit the crime or otherwise prevents the completion of the crime, shall not be liable for punishment under this Statute for the attempt to commit that crime if that person completely and voluntarily gave up the criminal purpose.

- 27.1 Irrelevance of official capacity. This Statute shall apply equally to all persons without any distinction based on official capacity. In particular, official capacity as a Head of State or Government, a member of a Government or parliament, an elected representative or a government official shall in no case exempt a person from criminal responsibility under this Statute… Immunities or special procedural rules which may attach to the official capacity of a person … shall not bar the Court from exercising its jurisdiction over such a person.

9. In 1999, The International Convention for the Suppression of the Financing of Terrorism was agreed Currently 188 States, including the UK

and the USA have ratified this treaty. Its main purpose is to halt the funding of terrorist acts. Article 2 states:

- Any person commits an offence if that person by any means, directly or indirectly, unlawfully and wilfully, provides or collects funds in the knowledge that they are to be used, in full or in part , in order to carry out any act intended to cause death or serious bodily injury to any other person when the purpose of such act is to intimidate a population, or to compel a government to do or to abstain from doing any act.

10. In 1946 the Nuremberg War Crimes Tribunal (1946) observed and held that:

- War is essentially an evil thing.Its consequences are not confined to the belligerent states alone, but affect the whole world. differing only from other war crimes in that it contains within itself the accumulated evil of the whole. To initiate a war of aggression therefore, is not only an international crime, it is the supreme international crime differing only from other war crimes in that it contains within itself the accumulated evil of the whole.

- Crimes against international law are committed by men, not by abstract entities, and only by punishing individuals who commit such crimes can the provisions of international law be enforced.

- Individuals have international duties which transcend the national obligations of obedience imposed by the individual State. He who violates the laws of war cannot obtain immunity while acting in pursuance of the authority of the State, if the State in authorising action moves outside its competence under international law.

Medical experiments on human subjects (the Nuremberg Code) require that:

- The voluntary consent of the human subject is absolutely essential… This requires that before the acceptance of an affirmative decision by the experimental subject there should be made known to him the nature, duration, and purpose of the experiment; the method and means by which it is to be conducted; all inconveniences and hazards reasonably to be expected; and the effects upon his health or person which may possibly come from his participation in the experiment. The duty and responsibility for ascertaining the quality of the consent rests upon each individual who initiates, directs or engages in the experiment. It is a personal duty and responsibility which may not be delegated to another with impunity…

Collecting or paying tax is a crime when the money is used for a criminal purpose.

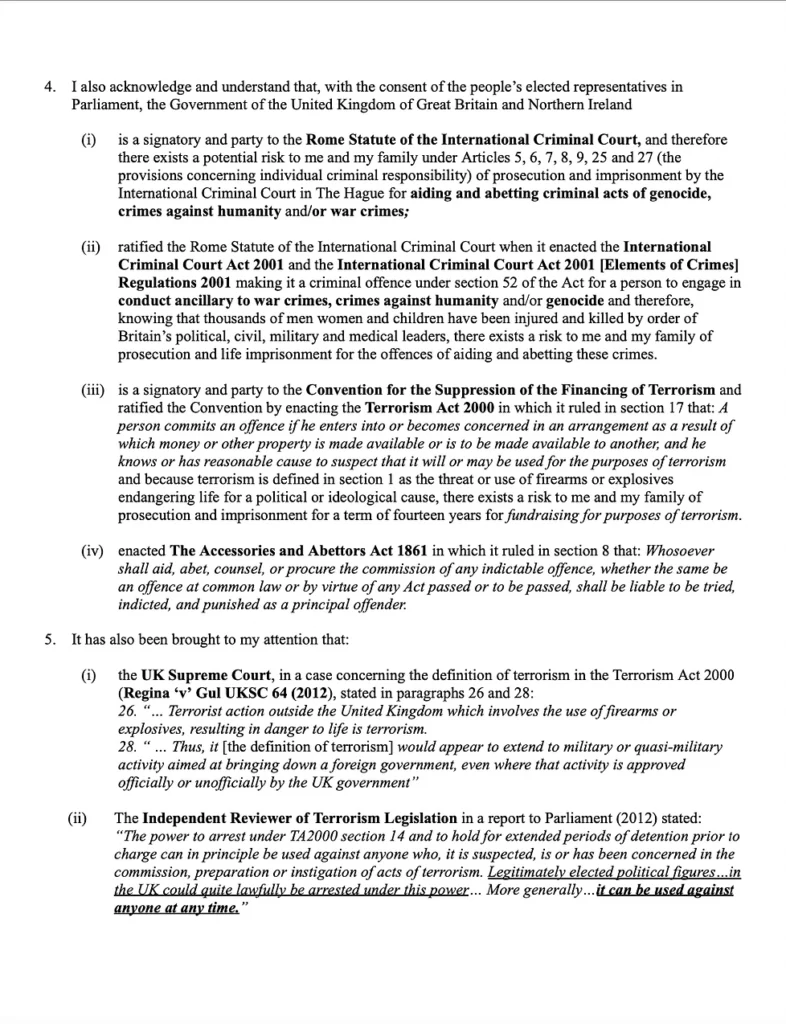

Domestic UK criminal law governing warfare, genocide and their funding:

11. In 1946 the UK Government ratified the United Nations Charter by enacting the United Nations Act 1946. This Act endorsed the prohibition

on the use of armed force and required the Monarch, as commander-in-chief of Britain’s military forces, to authorise by order in Council

their deployment on UN Security Council peacekeeping activities.

- Measures under Article 41. If, under Article forty-one of the Charter of the United Nations… (being the Article which relates to measures not involving the use of armed force) the Security Council of the United Nations call upon His Majesty’s Government in the United Kingdom to apply any measures to give effect to any decision of that Council, His Majesty may by Order in Council make such provision… for enabling those measures to be effectively applied, including… provision for the apprehension, trial and punishment of persons offending against the Order.

- Every Order in Council made under this section shall be laid before Parliament; and if any provision made by the Order would, if it were included in an Act of the Scottish Parliament, be within the legislative competence of that Parliament, before that Parliament.

12. In 2001 the UK Government ratified the Rome Statute of the International Criminal Court by enacting the International Criminal Court Act, and the International Criminal Court (Scotland) Act . These two laws make it a criminal offence in the UK for any person to engage in war crimes, crimes against humanity, genocide or conduct ancillary to such crimes. The International Criminal Court Act 2001 stipulates:

51. Genocide, crimes against humanity and war crimes. It is an offence against the law of England and Wales for a person to commit

genocide, a crime against humanity or a war crime.

52. It is an offence against the law of England and Wales for a person to engage in conduct ancillary to genocide, a crime against humanity

or a war crime …

55. Meaning of “ancillary offence”. References in this Part to an ancillary offence under the law of England and Wales are to—

(a) aiding, abetting, counselling or procuring the commission of an offence,

(b) inciting a person to commit an offence,

(c) attempting or conspiring to commit an offence, or

(d) assisting an offender or concealing the commission of an offence.

66. Mental element … a person is regarded as committing such an act or crime only if the material elements are committed with intent

and knowledge. … A person has intent in relation to conduct, where he means to engage in the conduct, and in relation to a consequence,

where he means to cause the consequence or is aware that it will occur in the ordinary course of events; and “knowledge” means

awareness that a circumstance exists or a consequence will occur in the ordinary course of events.

78. Crown application. This Act binds the Crown and applies to persons in the public service of the Crown, and property held for the

purposes of the public service of the Crown, as it applies to other persons and property.

13. The International Criminal Court Act 2001 [Elements of Crimes] Regulations specify in the four elements of genocide that must be proved

beyond reasonable doubt in court if a jury is to find a person guilty of the crime:

- The perpetrator killed or caused the death of one or more persons.

- Such person or persons belonged to a particular national, ethnical, racial or religious group.

- The perpetrator intended to destroy, in whole or in part, that national, ethnical, racial or religious group as such.

- The conduct took place in the context of a manifest pattern of similar conduct directed against that group or was conduct that could itself effect such destruction.

14. Parliament ratified the Convention of the Suppression of the Financing of Terrorism by enacting the Terrorism Act 2000 in which it ruled

in sections 1, 15, 17 and 19 that:

- Terrorism is the threat or use of firearms or explosives endangering life for a political or ideological cause,

15. (1) A person commits an offence if he invites another to provide money or other property and intends that it should be used, or has reasonable

cause to suspect that it may be used, for the purposes of terrorism.

(2) A person commits an offence if he receives money or other property and intends that it should be used, or has reasonable cause to suspect

that it may be used, for the purposes of terrorism.

(3) A person commits an offence if he receives money or other property and knows or has reasonable cause to suspect that it will or may be

used for the purposes of terrorism.

(4) In this section a reference to the provision of money or other property is a reference to its being given, lent or otherwise made available,

whether or not for consideration.

17. A person commits an offence if he enters into or becomes concerned in an arrangement as a result of which money or other property is

made available or is to be made available to another, and he knows or has reasonable cause to suspect that it will or may be used for the

purposes of terrorism.

19. Disclosure of information: Duty.

(1) This section applies where a person believes or suspects that another person has committed an offence under any of sections 15 to 18, and bases

his belief or suspicion on information which comes to his attention in the course of a trade, profession or business, or in the course of his

employment …

(2) A person commits an offence if he does not disclose to a constable as soon as is reasonably practicable his belief or suspicion, and the information on which it is based.

15. In 1861 Parliament enacted The Accessories and Abettors Act in which it ruled that:

8. Whosoever shall aid, abet, counsel, or procure the commission of any indictable offence, whether the same be an offence at common law or by

virtue of any Act passed or to be passed, shall be liable to be tried, indicted, and punished as a principal offender.

16. It has been brought to our attention that the UK Supreme Court, in a case concerning the definition of terrorism [Regina ‘v’ Gul UKSC 64 (2013)]), stated that:

- 26. Terrorist action outside the United Kingdom which involves the use of firearms or explosives, resulting in danger to life is terrorism.

- 28. Thus, it [the definition of terrorism] would appear to extend to military or quasi-military activity aimed at bringing down a foreign government, even where that activity is approved officially or unofficially by the UK government”

17. The Independent Reviewer of Terrorism Legislation (David Anderson KC) in a report to Parliament (2012) stated that:

- “The power to arrest under the Terrorism Act 2000 section 14 … can in principle be used against anyone who, it is suspected, is or has been concerned in the commission, preparation or instigation of acts of terrorism. Legitimately elected political figures…in the UK could quite lawfully be arrested under this power… More generally… it can be used against anyone at any time”.

The Crimes

18. It has also been brought to our attention that all taxes, fees, fines, duties, charges and payments of money to the Primary Beneficiary including

PAYE and NI contributions are paid into Parliament’s Consolidated Fund, whereupon some of this money is used by the Primary Beneficiary

directly and/or indirectly, in whole or in part, for illegal and criminal purposes, in particular to finance the manufacture, purchase, supply

and/or use by:

- The UK Ministry of Defence and HM Military Forces of weapons such as nuclear and high-explosive bombs, rockets, missiles and firearms as well as weapon delivery systems such as ships, aircraft, tanks, submarines and drones, for the instigation, facilitation, support or conduct of various illegal wars, invasions, occupations or armed attacks on the people of diverse independent Sovereign States, most recently Afghanistan, Iraq, Libya, Syria, the Yemen, Palestine and the Ukraine, causing serious bodily injury or death to thousands of innocent men, women and children, none of whom were given the opportunity to plead for their lives and the lives of their family in court before being summarily injured or killed by the actions of HM military forces by order of Britain’s political, civil, judicial and military commanders.

- The UK Home Office and UK police forces of firearms which may be used to threaten, harm or kill UK residents nationals and/or visitors;

- The Department of Health and Social Care. the National Health Service, Public Health England, The National Health Security Agency, MHRA, UK Ministers of State, civil servants, employees, advisors and members of the medical profession of experimental gene therapy falsely and deceptively described as safe and effective vaccines and administered without their informed consent to millions of UK residents and nationals resulting in harm, serious injury or death to tens of thousands of children, women and men.

Declaration of Conditional Trust

19. In the premise, we therefore declare and say that we shall transfer all money (taxes) deducted from employees’ salaries and wages in lieu of

PAYE and NI contributions and cause the same together with our employer’s contribution to be held until the last day of the financial year in

a conditional, revocable trust for Parliament, HM Government, HMRC or their agents (hereinafter known as the Primary Beneficiary).

THE TRUSTEES:

The following persons have agreed to act as Trustees of this Trust until __/__/____

20. On or before the last day of the financial year (5th April) our Trustees will meet to review the actions of the Primary beneficiary and the rulings of the International Criminal Court and the International Court of Justice in order to decide whether or not the conditions of the Trust specified in paragraph 24 below have been met to their satisfaction.

21. If all the conditions of this Trust have been met to the satisfaction of the Trustees, on or before the last day of the financial year, and they have received confirmation that the Primary Beneficiary is acting lawfully and legally in full accordance with international law and the articles of the UN Charter as well as all 42 principles in the UN Declaration on Principles of International Law (UNGAR 2625), then the trustees will pay the proceeds of the Trust in full to the Primary Beneficiary within 14 days of the last day of the current financial year (19th April 20__).

22. If the trustees find that the conditions of this Trust have not been met to their satisfaction and the Primary Beneficiary is continuing to use taxpayers’ money to fund, support, plan or take part in illegal or criminal acts of terrorism, warfare, crimes against humanity or genocide, then the Primary Beneficiary’s alleged right and claim to the money (taxes) will be automatically revoked and the trustees will arrange with the company [the Settlor] to return the money, together with the employer’s contribution, to the individual employees [the Secondary Beneficiary] from whose salary or wages the money was deducted. [NB. Employees can then make their own decisions as to how much of their money they will invest in the company’s pension fund and/or a personal pension fund.]

23. If the Trustees’ review of the Trust conditions indicates that the Primary Beneficiary is continuing to wage or support wars or the use of armed forces in violation of the world’s most important laws and they discover that the directors of the company are continuing to transfer money or property to the Primary Beneficiary in violation of Sections 15-18 of the Terrorism Act 2000, it is their legal duty under Section 19 of the Terrorism Act 2000 to report this information and the transgressors to the police. Should they fail to do so, they commit a criminal offence and may render themselves, as well as the directors and members of the company, liable to arrest, prosecution, conviction and imprisonment.

Trust Conditions

24. We further declare and say that , prior to the end of the financial year, the directors of the company and/or the Trustees receive incontrovertible documentary evidence from the International Criminal Court and/or the International Court of Justice and/or others that the Primary Beneficiary:

- has ended all involvement in the criminal acts identified at paragraph 18 above;

- is acting in full accordance with the UN Charter, the UN Declaration on Principles of International Law and the Laws specified in paragraphs 6-17 above;

- has ensured that criminal proceedings against at least 1000 of the leading instigators, perpetrators, financiers, bankers, investors, advisors, company directors, public officials and natural persons complicit in the criminal acts of the Primary Beneficiary identified at paragraphs 2, 3, 4 and 18 above.

We confirm that we shall recommence the collection and periodic payments to the Primary Beneficiary of employees’ PAYE and NI contributions and employers’ NI contributions in consideration of all lawful, legal and legitimate demands made upon us.

[N.B. Article 25.3(f) of the Rome Statute of the ICC (see para 8 above) provides a GET OUT OF JAIL FREE CARD for anyone involved in current crimes (such as funding genocide and crimes against humanity in Ukraine and Palestine) provided that THEY END THEIR INVOLVEMENT IN THE CRIME(S) NOW and they ACT to prevent their completion.]

The Trustees:

The following persons have agreed to act as Trustees of this Trust until __/__/20__

Trustees’ Duties

- On or before the last day of the financial year (5th April) our Trustees will meet to review the actions of the Primary Beneficiary in order to decide whether the conditions of this Trust specified in paragraph 20 above have been met to their satisfaction.

- If the trustees’ review of the trust conditions indicates that the Primary Beneficiary is continuing to wage or support wars or the use of armed force in violation of the world’s most important laws, and they discover that the directors of the company are continuing to transfer money or property to the Primary Beneficiary in violation of , it is their legal duty under to report this information and the transgressors to the police. Should they fail to do so they commit a criminal offence and may render themselves, as well as the directors and members of the company liable to arrest, prosecution, conviction and imprisonment.

Implications if Trust Conditions are not met:

- If on the last day of the financial year the trustees find that the is continuing to breach the domestic and international laws governing warfare, terrorism, genocide and/or crimes against humanity identified at paragraphs 6 – 17 above, and is continuing to take part in the criminal acts identified at paragraphs 2, 3, 4 and 18 above, and is thereby complicit in the criminal offences of murder, misconduct in public office, misfeasance, crimes against peace, war crimes, crimes against humanity and/or genocide, then they are required to revoke this Trust and to return the PAYE and NI contributions plus employers NI contributions to their employees (the Secondary Beneficiary).

Signed this [ ] day of [ ] 2023

for and on behalf of the Company by ___________________________________ [ __________________________________________ ]

signature print name

Director

for and on behalf of the Company by ___________________________________ [ __________________________________________ ]

signature print name

Director / Company Secretary

Questions and Answers

How do I fill in the form?

Add your name address etc and in the tax ‘Consent to Pay’ line, add the total amount of Taxes & Fines you are consenting to pay so long as the government can guarantee your demands and show they are not involved in any criminal activity.

What do I do with the form?

Get it witnessed and keep a couple of originals. Send a copy to each speculator who claims you owe them money. There are some sample letters available on this site, though it’s always best to make the words your own as the councils respond better to individual letters.

What will happen next?

If you receive further correspondence, always be polite and stand your ground. Remember, it is not illegal or unlawful to withhold tax (after all, many MPs & oligarchs do exactly that – tax avoidance as opposed to tax evasion – and we are all equal under the law) and you are not willfully refusing to pay tax (this is important) you are effectively paying your taxes and fines by putting the money into a trust, with the government as Primary Beneficiary (you are both Trustee and Settler – the one who settles the fines/taxes). The government can collect whenever it can prove it has not been involved in any criminal activity.

Can I use this to hold money for my kids in trust?

No. This is specifically a Declaration of Sovereignty and Deed of Discretionary Revocable Conditional Trust and Withdrawal of Consent to Illegal Taxation. You would need to talk to a lawyer (or accountant) to set up a Trust for your children.

What happens at the end of the tax year?

If by the end of the tax year the government is able to show it has ceased to be involved in any illegal activity, then you pay the taxes to the government. If the government is not able to show this, you get to keep your money. Presently, it is highly unlikely that the government will comply with your lawful conditions. You can then apply your money to local causes that satisfy your civic duty.

But if I don’t pay Council Tax, who will pay for the local amenities, like buses and the library?

In the first instance the important thing is not to fund wars. No funding, no wars. Once you have committed to forcing the government to behave responsibly, it either will (unlikely) or cannot (likely). You and a collective of local residents can set up a Community Co-operative Taxation Trust in which your taxes can be paid and you can help finance your local community. Imagine the savings if you don’t have to pay council heads £250,000 and other spurious costs.

What if I’m not self-employed and my employer automatically deducts NI and PAYE?

You need to inform your employer that when Britain signed up to the United Nations Charter, the Rome Statute, the International Criminal Court and Nuremberg, they had a duty to honour these solemn and binding agreements made between nation States. As they have not, it is up to every one of us to honour what was agreed, including to resolving all disputes peacefully and never intervening directly or indirectly – for whatever reason – in the external or internal affairs of any other state. It is contrary to the Nuremberg Code to initiate a war of aggression – the supreme international crime.

Does the Primary Beneficiary Need to Sign the Deed of Declaration?

No. The Primary Beneficiary doesn’t need to sign. This is not a contract. It is very similar to a living Will. The beneficiaries of Will don’t need to agree to the Will. All they need to know is that they are beneficiaries and if there are conditions attached to the will then they need to know them so that they can choose whether to meet them or not.

In your PAYE sample, you have included every employee within the company. Can this instead be done for the individual only and not every employee?

It can. I put all employees because it will be beneficial to all employees and especially to the directors who have to authorise it.

But if I haven’t given the HMRC any money, how have I paid?

Once you have completed the Trust document and had it witnessed and put 10% of the tax debt (in cash, post-dated cheque or a promissory note) aside in a folder labelled Trustee and have sent copies of the Trust Deed to HMRC and the Council, you have PAID YOUR TAXES.

On 5/4/24 you need to check whether the Government has met your conditions. If it has then start paying the taxes. If it hasn’t, then write to HMRC and the Council formally revoking their right to claim any back taxes from you and set up a new Declaration and Deed of Conditional Trust for the year ahead. But make sure you never again send them any money in lieu of taxes. Because if you do you will be committing a criminal offence under sections 15 and 17 of the Terrorism Act 2000 and section 52 of the International Criminal Court Act 2001 and if found guilty you could be sent to prison for 14 or 30 years respectively.

Chris Coverdale – Lawfully Opting Out of Taxation – Introduction – YouTube

923 wyświetlenia 19 mar 2023Presented by: Chris Coverdale Narrated by: Nathaniel Wills Link to documents mentioned within this video: /drive/folders/1w49bSqUFWNJcUtu0Gxd975220jMA_47H (Type https:// drive.google.com first, then paste the above after it, alternatively, read my pinned comment within the comments section for the full link.)

Chris Coverdale – Lawfully Opting Out of Taxation – Introduction – YouTube

https://drive.google.com/drive/folders/1w49bSqUFWNJcUtu0Gxd975220jMA_47H

Here you can see first two docs.

Renovation and restoration

Experience the fusion of imagination and expertise with Études Architectural Solutions.

Continuous Support

Experience the fusion of imagination and expertise with Études Architectural Solutions.

App Access

Experience the fusion of imagination and expertise with Études Architectural Solutions.

Consulting

Experience the fusion of imagination and expertise with Études Architectural Solutions.

Project Management

Experience the fusion of imagination and expertise with Études Architectural Solutions.

Architectural Solutions

Experience the fusion of imagination and expertise with Études Architectural Solutions.

Claim all taxes

Leave a Reply